Nigeria’s economy expanded by 3.89 percent in the first quarter of 2026, according to the latest GDP report released by the National Bureau of Statistics on Monday, broadly in line with BusinessDay Economics’ April projection of 4.0 percent, with a marginal deviation of 0.11 percentage points. The outcome reinforces a growing view among economists that Nigeria’s reform programme is beginning to deliver measurable economic gains.

But the most consequential detail in the report was not the headline figure. It was the shift in the underlying drivers of growth.

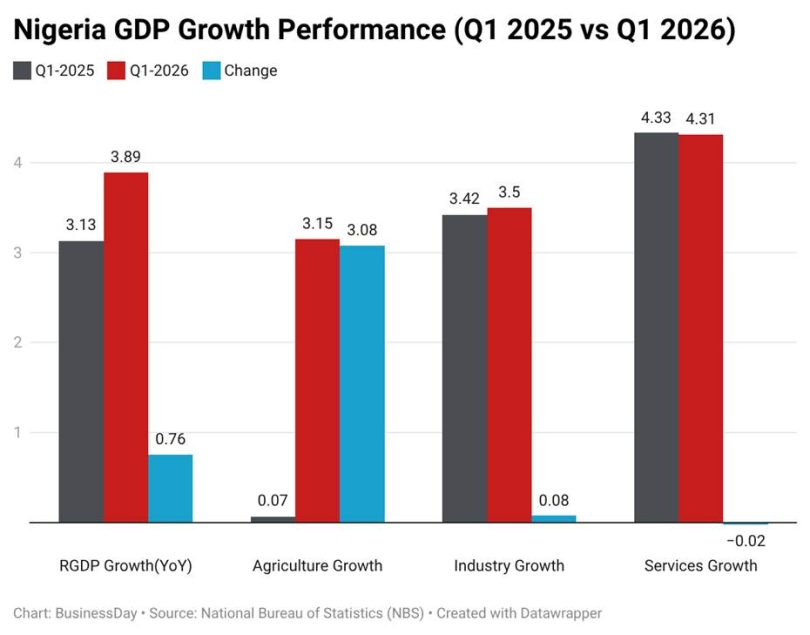

For much of the past three years, agriculture had been one of the weakest links in Nigeria’s economic performance, constrained by insecurity, rising input costs and persistent disruptions across key farming regions. Historical data in the report show agricultural output expanded by just 0.07 percent in Q1 2025, effectively stagnating in a sector that remains one of the country’s largest employers.

The latest numbers mark a decisive reversal.

Agriculture rebounded to 3.15 percent in Q1 2026, emerging as one of the strongest turnaround stories within the real economy and helping to broaden growth beyond its recent narrow base. But it was not the only driver.

Read also: The Nigeria policy watch – Policy, performance & accountability

A more balanced growth profile

The recovery was underpinned by a more even performance across major sectors. Industry expanded by 3.50 percent, slightly above the 3.42 percent recorded a year earlier, reflecting modest gains in manufacturing, construction and related activities.

Services, which remains the dominant engine of the economy, grew by 4.31 percent, broadly stable compared to 4.33 percent in Q1 2025, but continued to account for the largest share of output at 57.73 percent, marginally higher than 57.50 percent in the previous year.

Together, these figures point to an economy that is not relying on a single engine of growth. Instead, recovery is increasingly being shaped by a combination of agricultural rebound, steady industrial expansion and sustained services resilience.

Why the agricultural rebound matters

The significance of agriculture’s recovery extends beyond output statistics.

The sector remains deeply embedded in Nigeria’s economic structure, not only as a contributor to GDP but as a primary source of livelihoods. According to World Bank estimates, around 35 percent of Nigeria’s labour force is employed in agriculture, underscoring its outsized role in household income distribution and rural economic stability.

Unlike services or oil, its transmission effects are direct, flowing through food supply, rural incomes, employment and consumption patterns.

When agriculture weakens, the impact is quickly reflected in food inflation and household strain. When it strengthens, it eases supply bottlenecks and supports broader macroeconomic stability.

In that context, the latest data suggest more than a cyclical improvement. They indicate a sector that is beginning to shift from being a drag on growth to a stabilising force within the economy.

Read also: The ‘Jollof Index’ and Nigeria’s cost-of-living collapse

Three years after reform shocks, signs of stabilisation

The first-quarter data arrive nearly three years after a series of structural policy shifts that reshaped Nigeria’s economic landscape, including fuel subsidy removal, exchange-rate liberalisation and sustained monetary tightening.

The immediate effects were severe. Inflation accelerated sharply, business costs rose, and household purchasing power came under sustained pressure. At the time, questions intensified over whether the reforms would eventually translate into durable growth.

The latest report does not settle that debate, but it strengthens the case that the adjustment phase is maturing.

GDP growth has now steadily improved from 2.31 percent in Q1 2023 to 2.98 percent in 2024, 3.13 percent in 2025 and 3.89 percent in 2026. The consistency of this trajectory, despite multiple shocks, suggests the economy may be transitioning from stabilisation into an early recovery phase.

Growth is improving, but transformation remains limited

Despite stronger headline performance, the structure of growth remains largely unchanged.

Services continue to dominate the economy, accounting for 57.73 percent of GDP, while industry has yet to show a meaningful structural acceleration. Manufacturing and broader industrial activity remain constrained relative to the scale needed for deep productivity gains.

This matters because sustained income growth is rarely driven by services alone. Industrial expansion typically anchors job creation, strengthens domestic value chains and deepens economic resilience.

The latest data therefore point more to resilience in existing structures than to structural transformation.

Why it matters for investors

For investors, the report offers a more nuanced signal than the headline figure suggests.

The broadening of growth across agriculture, industry and services reduces concerns about excessive concentration in a narrow set of sectors. The agricultural rebound, if sustained, could help ease food inflation pressures and improve real household incomes, with spillover effects into consumption-driven sectors.