…Inflation climbs for second straight month in April

…As U.S/Iran war reverses disinflationary trend

The Monetary Policy Committee (MPC) of the Central Bank of Nigeria (CBN) is facing severe pressure to maintain the benchmark interest rate at its upcoming meeting. Renewed geopolitical volatility in the Middle East has heightened global inflation fears, complicating the domestic macroeconomic outlook and forcing policymakers into a cautious stance.

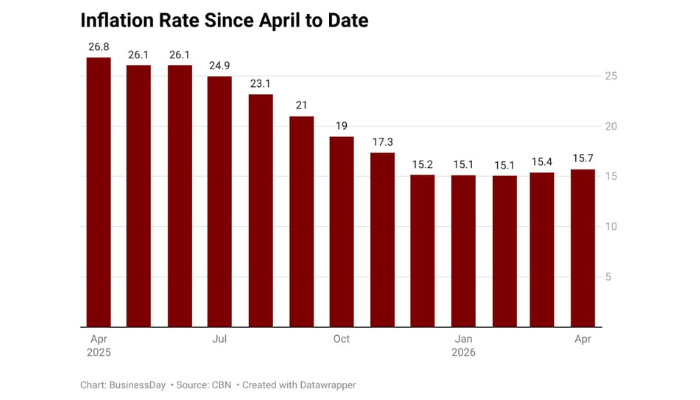

On Tuesday, Olayemi Cardoso, governor of the CBN, will chair the committee’s second session of the year. Eight economists and market analysts polled by BusinessDay expect the committee to hold the Monetary Policy Rate (MPR) steady at 26.5 percent. This consensus underscores a growing need to preserve foreign exchange stability and monitor resurgent inflationary pressures before altering borrowing costs. Last week, Nigeria’s headline inflation rose to 15.69 percent in April 2026, up from 15.38 percent in March, stoking expectations that interest rates will remain unchanged.

The MPC at its 304th meeting held on February 23 and 24, 2026, had reduced the benchmark interest rate by 50 basis points to 26.5 percent, while retaining the asymmetric corridor around the MPR at +50/-450 basis points. The committee also retained the Cash Reserve Ratio (CRR) for Deposit Money Banks at 45 percent, Merchant Banks at 16 percent and 75 percent for non-TSA public sector deposits.

Since that decision, escalating tensions involving the United States, Israel, and Iran have triggered fresh volatility across global energy and logistics markets. The resulting increase in fuel prices threatens a rapid inflation pass-through into the broader economy.

Read also: CBN fixes May 19–20 for 305th MPC meeting after February rate cut

Razia Khan, managing director and chief economist for Africa and the Middle East at Standard Chartered Bank, said Nigeria’s inflation expectations remain weakly anchored despite reforms in the foreign exchange market and fuel subsidy removal.

“Nigeria is an oil producer with refining capacity, but the recency of its fuel subsidy and FX reforms suggests that inflation expectations are not well anchored,” Khan said.

According to her, March inflation accelerated by 4.2 percent month-on-month as fuel price increases filtered rapidly into other components of the consumer price index, including services. She said Standard Chartered now expects the CBN to hold the policy rate at 26.5 percent while investors closely watch for signals of possible future tightening.

Muda Yusuf, chief executive officer of the Centre for the Promotion of Private Enterprise (CPPE), said the MPC’s deliberations would also be shaped by geopolitical risks, domestic liquidity pressures and election-related spending ahead of the 2027 political cycle.

He noted that increased political spending, combined with improved Federation Account Allocation Committee (FAAC) disbursements to states, could heighten excess liquidity conditions and complicate inflation management.

“The MPC is therefore likely to assess these developments through the lens of its price stability mandate and inflation-targeting framework,” Yusuf said.

He warned, however, that further monetary tightening could weaken economic growth, suppress private sector investment and worsen financing conditions for businesses.

According to him, the current inflationary pressures are largely cost-push and supply-side driven, stemming from energy costs, exchange rate pass-through, logistics bottlenecks and structural inefficiencies, factors that are less responsive to aggressive monetary tightening.

Ayodele Akinwunmi, chief economist at United Capital, expects a hold, saying that while the U.S.–Iran conflict has heightened inflation risks in Nigeria and several other economies, the Monetary Policy Committee’s (MPC) policy tools remain constrained as the pressures are largely supply-driven rather than demand-led.

He noted that, given the relative stability in the foreign exchange market, maintaining the key policy rate is crucial at this stage. However, he said the MPC may consider adjusting the Cash Reserve Ratio (CRR) on non-TSA public sector deposits to 85 percent from 75 percent in a bid to mop up additional liquidity from the financial system.

Read also: Investors still bet big on T-bills post-MPC rate cut

Ayokunle Olubunmi, head of Financial Institutions Ratings at Agusto & Co, also expects rates to remain unchanged. He said inflationary risks tied to the Middle East crisis would likely discourage the MPC from considering another rate cut.

Tunde Abidoye, head of research at Quest Merchant Bank, said the balance of economic indicators supports a cautious policy stance.

“We are already seeing an uptick in inflationary pressures, partly driven by global developments,” Abidoye said. “Central Banks such as the US Federal Reserve and the European Central Bank are holding rates steady amid rising price pressures and geopolitical shocks, particularly from the Middle East.”

He added that easing rates in Nigeria at this point could narrow the interest rate differential with advanced economies and potentially weaken foreign portfolio inflows.

Olufunmilola Adebowale, head of research at Parthian Partners, said the MPC’s decision would likely be influenced by the April inflation figures, which rose to 15.69 percent recently.

While monthly inflation may moderate after the sharp energy-driven increase recorded in March, she said the development should be viewed more as a normalisation rather than evidence of a sustained disinflation trend.

“Against this backdrop, we expect the committee to maintain a cautious stance, opting for a wait-and-see approach,” Adebowale said.

Olanrewaju Kazeem, group chief executive officer of Alert Group, said several factors will influence the direction of the Monetary Policy Committee (MPC) in determining the Monetary Policy Rate (MPR), including inflation dynamics, global geopolitical tensions, and domestic liquidity conditions.

He noted that the slight increase in inflation from 15.1 percent in January to 15.38 percent in April reflects the impact of the Middle East crisis involving Iran, Israel and the United States, adding that the possible resolution or escalation of the conflict will significantly shape economic conditions and policy direction.

“Generally, interest rates across major global economies appear relatively stagnant, largely due to uncertainty and unpredictability surrounding the outcomes of the war,” Kazeem said.

Read also: What the MPC’s rate cut really signals

“The improved FX inflow, stability of the naira and the recent gradual appreciation of the currency could support a stable or reduced rate to encourage economic growth while preserving exchange rate stability. Overall, a cautious wait-and-see approach is expected, where the rate remains unchanged or sees a minor reduction to stimulate the economy. The activities of the Strait of Hormuz will determine how straight things could be.”