In 2025, Nigeria’s biggest banks recorded growth in customer deposits, assets, equity, and revenue, reflecting continued liquidity expansion across the financial system as high interest rates and monetary tightening reshaped banking operations.

According to the audited financial statements for the year ended December 31, 2025, First HoldCo, Guaranty Trust Holding Company, Zenith Bank, United Bank for Africa (UBA), and Access Holdings Plc showed that combined customer deposits rose to N114 trillion from N93 trillion reported in 2024.

This shows that lenders continued to attract deposits and expand balance sheets despite slower loan growth.

The performance comes at a time when the Central Bank of Nigeria (CBN) maintains a tight monetary policy stance to curb inflation and stabilise the foreign exchange market.

The MPR was slashed by 50 basis points to 26.5 percent in February 2026, following five months of declining inflation. The MPC recently reduced the Cash Reserve Ratio (CRR) by 500 basis points (from 50 percent to 45 percent) to facilitate some easing in the economy.

Deposit growth strengthens liquidity position

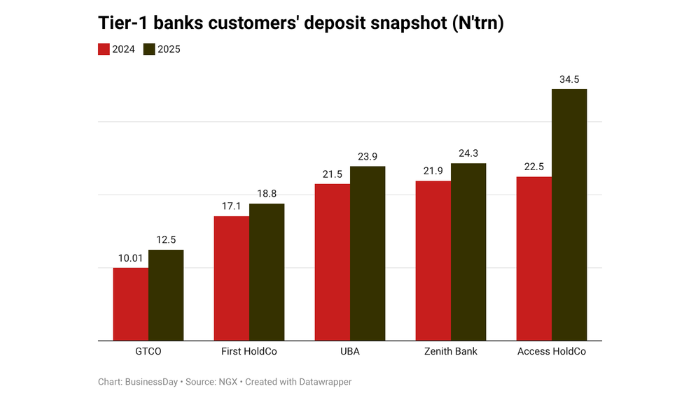

Customer deposits across the five biggest banks increased by 23 percent within one year, highlighting sustained confidence in the banking sector and increased liquidity within the financial system.

Access Holdings recorded the largest growth in deposits among the banks reviewed. Customer deposits rose to N34.5 trillion in 2025 from N22.5 trillion in 2024, while total assets expanded to N51.5 trillion from N41.4 trillion, supported partly by the integration of newly acquired subsidiaries.

UBA grew customer deposits to N23.9 trillion from N21.5 trillion and increased total assets from N30.3 trillion to N33.7 trillion during the period.

Zenith Bank’s deposits rose to N24.3 trillion from N21.9 trillion, while total assets increased to N31.4 trillion from N29.9 trillion.

First HoldCo recorded customer deposits of N18.8 trillion in 2025 compared to N17.1 trillion in 2024, while assets rose from N26.5 trillion to N27.1 trillion.

GTCO expanded deposits to N12.5 trillion from N10.01 trillion and increased assets to N17.7 trillion from N14.7 trillion.

Although banks expanded their loan books in 2025, Data obtained from the Financial Markets Dealers Association (FMDA) showed that banking system liquidity rose to N4.15 trillion as of April 2026. This marks a 1,253.06 percent increase compared to the N306.54 billion recorded in April 2023, the year the CBN first announced the programme.

The recapitalisation drive, which concluded on 31 March 2026, has fundamentally reshaped industry balance sheets. Banks raised over N4.65 trillion over 24 months to meet new capital requirements. Despite this liquidity surge, credit to the private sector has expanded at a more moderate pace.

Lending rose by 0.9 percent month-on-month to N94.61 trillion in February 2026, compared to N93.74 trillion in January. On a year-on-year basis, credit grew by 24.06 percent from N76.26 trillion in February 2025. This divergence highlights a growing disconnect between improved banking liquidity and the pace of credit flow to businesses.

Despite this, the pace of credit growth remained below the increase in customer deposits.

Loan growth across the lenders remained moderate. Access Holdings increased loans and advances from N11.4 trillion to N13.3 trillion, while Zenith Bank expanded lending from N9.96 trillion to N10.4 trillion.

First HoldCo’s loans rose from N8.76 trillion to N9.06 trillion, while UBA increased lending from N6.95 trillion to N7.02 trillion. GTCO grew loans and advances from N2.78 trillion to N3.12 trillion.

This trend led to a moderation in loan-to-deposit ratios across the banking groups reviewed, indicating that lenders maintained more conservative lending positions despite stronger liquidity.

The loan-to-deposit ratio (LDR) is a key financial metric used to assess a bank’s liquidity by comparing its total loans to its total deposits, expressed as a percentage. It measures how much of a bank’s deposits are funded by loans,

Access Holdings’ loan-to-deposit ratio declined to 38.6 percent in 2025 from 50.7 percent in 2024, as deposit growth significantly outpaced loan expansion.

First HoldCo’s ratio fell to 48.2 percent from 51.2 percent, while Zenith Bank’s ratio declined from 45.5 percent to 42.8 percent.

UBA’s loan-to-deposit ratio moderated from 32.3 percent to 29.4 percent, while GTCO recorded the lowest ratio among the banks reviewed, declining to 25 percent from 27.8 percent.

Capital position improves amid recapitalisation push

Nigerian banks are expected to significantly increase lending in 2026 as stronger capital positions following the industry-wide recapitalisation exercise provide room for fresh credit expansion, according to Fitch Ratings.

The global ratings agency said nominal loan growth in the banking sector is projected to accelerate to more than 20 percent in 2026 after slowing sharply to about 5 percent in 2025 due to tight monetary conditions, high interest rates and the withdrawal of regulatory forbearance measures.

Fitch said the fresh capital raised by banks to meet the Central Bank of Nigeria’s new paid-in capital requirements has strengthened balance sheets and positioned lenders for business growth.

“All Fitch-rated licensed Nigerian banks have met the new paid-in capital requirements effective from the end of the first quarter (Q1’26), as have the majority of non-rated banks,” Fitch said.

A review of the tier one banks’ financial statements revealed that combined equity for the five lenders rose to N19.5 trillion in 2025 from N16.3 trillion in 2024.