For three years, Nigeria’s reform programme has rested on a difficult political bargain: households absorb short-term pain today in exchange for the promise of a more stable economy tomorrow.

That bargain is now under renewed strain.

Just as policymakers and investors were beginning to believe the worst of the adjustment phase had passed, inflation has started to edge upward again. The concern is not only that prices are rising, but that the reversal is arriving before most households have experienced meaningful relief from years of adjustment.

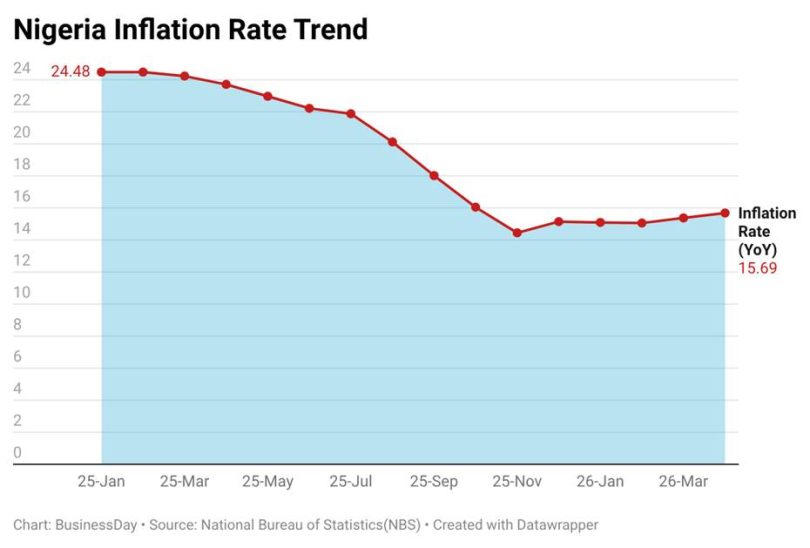

For eleven consecutive months, the data pointed in the opposite direction. Headline inflation eased to 15.06 percent in February 2026, down from peaks above 33 percent during the most intense phase of post-reform pressures in 2024. According to Central Bank Governor Olayemi Cardoso, the moderation reflected lagged effects of monetary tightening, improved exchange-rate stability, and temporary improvements in food supply conditions.

For a moment, it appeared the economy was turning a corner.

That shift in sentiment was visible in policy and markets. The Central Bank cut its benchmark interest rate by 50 basis points to 26.5 percent in early 2026, its first reduction in years. External reserves rose to $50.4 billion, the highest level in over a decade. Together, falling inflation, stronger reserves, and improved FX stability strengthened the narrative that Nigeria was entering a post-adjustment phase.

Then the external environment changed.

The outbreak of conflict in the Middle East in February 2026 and disruptions to shipping through the Strait of Hormuz altered global energy dynamics. With roughly a fifth of global seaborne crude trade passing through the corridor, even partial disruption had outsized effects.

Global oil supply reportedly fell sharply in March, while Brent crude surged about 65 percent within weeks, reaching $120.4 per barrel in April from $103.7 in March, according to BusinessDay.

For Nigeria, higher oil prices usually improve fiscal revenues and external balances. But the transmission has become less straightforward.

The economy remains heavily dependent on imported energy inputs, transport costs, and production-linked foreign exchange pressures. As a result, global oil price increases now generate a dual effect: stronger government inflows on one side, and higher domestic cost pressures on the other.

The net effect is often felt more in household budgets than in fiscal accounts.

That tension quickly reappeared in the inflation data.

Headline inflation rose from 15.06 percent in February to 15.38 percent in March, then to 15.69 percent in April. More importantly, food inflation crossed above headline inflation for the first time in eight months, reaching 16.06 percent.

This shift is significant. Food prices tend to capture the most immediate pressure on living standards, particularly in economies where households spend a large share of income on basic consumption. The previous period of food inflation moderation had been one of the strongest signals that conditions were stabilising.

That signal is now weakening.

Read also: Election-year inflation threatens Nigeria’s reform push, S&P says after upgrade

The composition of inflation shows a broadening cost base rather than a single-sector shock.

Food and non-alcoholic beverages contributed the largest share of headline inflation pressure, followed by restaurants, transport, and energy-related costs. Monthly energy inflation alone reached 8 percent, reinforcing the cost-push nature of the current cycle.

The pressure is also spatially uneven. Rural inflation reached 16.36 percent compared with 15.40 percent in urban areas, reflecting the sensitivity of agricultural supply chains to transport costs, insecurity, and input shortages.

According to Kola Masha, chief executive of Babban Gona, persistent rural cost pressures risk feeding directly into national food inflation, given the centrality of rural producers in Nigeria’s food system.

State-level data underscores the fragmentation. Inflation is significantly higher in parts of the north and southeast, with some states recording rates above 25 percent, while food inflation in certain regions exceeds 30 percent. These are not abstract statistics; they represent sharply divergent living conditions across the country.

Despite these pressures, financial markets continue to price a more stable outlook.

On May 15, 2026, S&P Global Ratings upgraded Nigeria’s sovereign credit rating from B- to B with a stable outlook, its first upgrade since the pre-pandemic period. The agency cited exchange-rate liberalisation, subsidy removal, improved external buffers, and structural fiscal reforms, including increased oil revenue remittance mechanisms.

S&P projected government revenue rising to 12.4 percent of GDP by 2026, alongside stronger growth and a sustained current account surplus. The World Bank has also maintained a positive medium-term growth outlook.

Abdulrauf Bello, a financial analyst, argues that such upgrades reflect macroeconomic stabilisation rather than immediate improvements in household welfare.

That distinction is becoming central to Nigeria’s reform story.

The Central Bank now faces a difficult balancing act.

Ahead of its May Monetary Policy Committee meeting, its inflation expectations survey showed that most respondents preferred a rate cut. This is understandable: borrowing costs remain high, with average lending rates to manufacturers still above 35 percent.