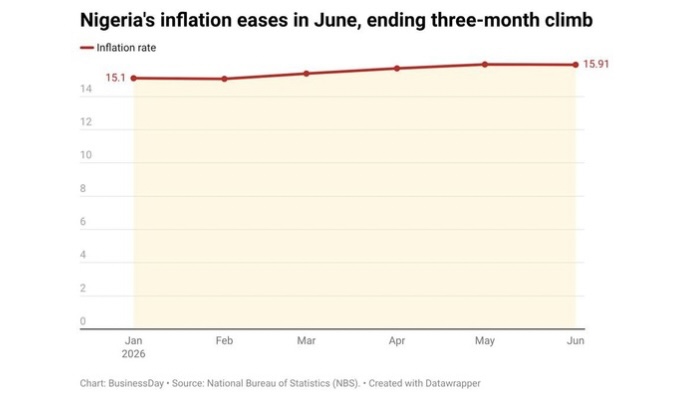

Nigeria’s inflation story is no longer about whether prices are rising or falling. It is increasingly about persistence. Headline inflation eased marginally to 15.91 percent in June from 15.93 percent in May, according to the National Bureau of Statistics (NBS), almost exactly matching BusinessDay’s 15.9 percent Inflation Nowcast published ahead of the official release. The difference was statistically negligible. The implication is not.

The latest reading suggests Nigeria may have entered a new phase of its inflation cycle. The rapid disinflation that followed last year’s rebasing exercise appears to have stalled, but neither has inflation resumed a meaningful upward march despite renewed geopolitical tensions and higher global oil prices.

That leaves policymakers confronting a far more difficult problem than the one they faced a year ago. After reaching a low of 15.06 percent in February, inflation rose steadily for three consecutive months before flattening in June. That pattern matters.

For most of the past year, economists debated whether inflation would continue falling. The June data suggests the debate has changed. Inflation is no longer falling meaningfully. It is settling around 16 percent. For the Central Bank of Nigeria, that is both reassuring and uncomfortable.

Reassuring because inflation has not reignited despite fresh external shocks. Uncomfortable because neither has it returned to a convincing downward trajectory that would justify aggressive monetary easing.

Read also: Nigeria’s reform execution test: Trust, food and factories after stabilisation

BusinessDay got the direction right

BusinessDay’s Inflation Nowcast projected inflation at about 15.9 percent, reflecting expectations that exchange-rate stability would offset renewed pressure from higher energy prices and supply constraints. The official reading of 15.91 percent broadly confirmed that assessment.

More importantly, it reinforces a broader conclusion that has been emerging over recent months: the nature of Nigeria’s inflation is changing. Between 2023 and early 2025, inflation was dominated by macroeconomic shocks. The removal of fuel subsidies. The liberalisation of the foreign exchange market.

The sharp depreciation of the naira. These were large one-off adjustments that rapidly fed through the economy. Those shocks are now fading. What remains are structural pressures that monetary policy cannot easily solve.

Food is becoming the bigger problem again

The headline number tells only part of the story. Food inflation accelerated to 17.52 percent year-on-year, while monthly food inflation climbed sharply to 3.75 percent, up from 2.98 percent in May. That divergence is important. Overall inflation may be stabilising, but food prices are rising faster again.

For households, food inflation matters far more than headline inflation. Food accounts for the largest share of household expenditure, particularly among lower-income Nigerians.

When food inflation accelerates, consumers rarely feel that inflation is slowing. This partly explains why public perceptions of inflation often differ sharply from official statistics.

Statistically, inflation has moderated dramatically from last year’s peak. Economically, many households still experience relentless increases in the prices that matter most.

The Central Bank has probably done most of what it can

Nigeria has experienced one of the most aggressive monetary tightening cycles in its modern history. The Monetary Policy Rate rose from 11.5 percent in 2022 to 27.5 percent before being reduced slightly to 26.5 percent. That tightening appears to have achieved its primary objective.

Exchange-rate volatility has moderated.

Inflation expectations have become more stable. Capital inflows have strengthened considerably. Foreign reserves have risen. The latest inflation reading suggests monetary policy has largely prevented another inflation spiral.

The challenge now is different. Higher interest rates cannot produce more food. They cannot reduce transport bottlenecks. They cannot solve insecurity affecting agricultural production. Nor can they lower electricity costs facing manufacturers. Those are increasingly the forces keeping inflation elevated.

The MPC’s decision has become easier

When the Monetary Policy Committee meets next week, the June inflation report gives policymakers little reason to move aggressively in either direction. An inflation rate of 15.91 percent is sufficiently stable to avoid another rate increase. At the same time, renewed food inflation and continued uncertainty surrounding global energy prices make an early rate cut difficult to justify.

The most likely outcome therefore remains another hold. Markets will probably pay less attention to the policy rate itself than to Governor Olayemi Cardoso’s guidance on what conditions would justify the first significant easing cycle.

The economy is entering a different phase

The most encouraging aspect of the June data is not that inflation fell by two basis points. It is that inflation appears to be stabilising despite fresh external pressures. That suggests Nigeria has largely moved beyond the acute macroeconomic adjustments triggered by the subsidy removal and exchange-rate liberalisation.

The economy is now entering a more difficult phase. The Central Bank has probably reached the limits of what interest rates alone can achieve. The next phase of Nigeria’s inflation fight will depend less on monetary policy than on whether the government can produce more food, move goods more cheaply and make businesses more productive. Inflation is no longer primarily a monetary problem. It is increasingly an economic one.