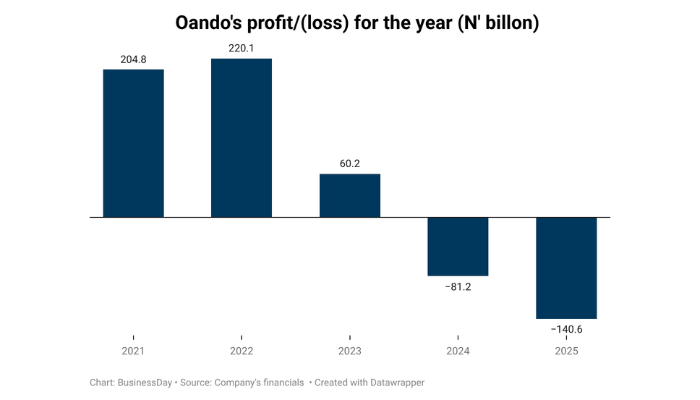

Oando Plc closed out 2025 with a headline profit of ₦204.8 billion, but the number obscures a company that its own auditors say may not survive the year ahead without emergency shareholder support.

Oando, one of Africa’s largest indigenous energy companies by assets, posted a 22 percent decline in revenue to N3.18 trillion in 2025 from N4.09 trillion a year earlier. Gross profit went negative to a N2.76 billion loss, meaning Oando lost money on the basic business of selling what it produces and trades, before a naira of overhead, interest or tax was counted.

Operating profit dropped by 58 percent to N241.0 billion from N569.7 billion, yet the company still reported a N204.8 billion profit after tax.

Further findings showed the bottom-line profit that Oando reported came almost entirely from a single, non-cash item of a N441.5 billion reversal of impairment on financial assets, an accounting adjustment that added nothing to the company’s cash and did nothing to fix what is breaking underneath it.

“The Group has a significant working capital deficiency and financing constraints,” the company’s auditor, BDO Professional Services, wrote in the notes to the accounts, adding that the conditions “indicate the existence of a material uncertainty that may cast significant doubt on the Group’s and Company’s ability to continue as a going concern.”

The auditors noted that its “Opinion is not modified in respect of this matter”.

At the parent-company level, the numbers look even stranger. Oando Plc reported N468.6 billion in profit for 2025, roughly four times the N111.8 billion booked in 2024, but on zero revenue.

The company recorded no revenue from contracts with customers at all during the year, compared with N343.9 billion in 2024. Nearly all of that parent-level profit came from other income and intercompany transactions rather than trading operations.

The oil company’s total group equity was negative N567.0 billion at year-end, worse than the negative N361.0 billion a year earlier, which may imply that Oando, on paper, owes more than it owns.

Net current liabilities, the gap between what the company must pay within a year and what it can lay hands on in that time, swelled to rN3.76 trillion. Cash on the balance sheet stood at ₦439.9 billion, a fraction of that gap.

Retained earnings have now been negative for five straight years, a run the company’s own five-year summary lays out without comment.

Oando’s auditors noted the Group achieved only 57.4 percent of budgeted production, measured in barrels of oil equivalent, and just 53 percent of budgeted revenue.

“This underperformance against budget adversely impacts on the Group’s ability to generate sufficient cash flows to meet its debt servicing obligations,” auditors said.

A closer look into the notes of the account showed Oando “defaulted on multiple borrowing arrangements across several financing facilities,” triggering events of default and forcing the reclassification of long-term debt into current liabilities.

On its Medium-Term Loan alone, the company could not meet a N113.6 billion obligation: N76.9 billion in principal, N21.1 billion in accrued interest, N8.7 billion in default interest and N6.9 billion in advisory fees.

Oando said lenders have not formally declared an event of default as of the report’s approval date, but they retain the right to do so and to enforce security pledged under a 2016 security deed.

“The Lenders have not issued an event of default as of the date of approval of these consolidated and separate financial statements. The Lenders may, in addition to the declaration of an event of default, seek to enforce their rights in the Security Deed dated 30 June 2016,” Oando said.

Oando auditors said the company’s own plan for staying afloat leans on related-party support.

For instance, a letter of guarantee, valid through March 2027, commits Ocean and Oil Development Partners Limited, Oando’s majority shareholder, to ensure the company and its subsidiaries can meet their obligations as they fall due.

“Management has prepared cash flow forecasts which assume continued operations and the successful execution of funding plans, supported by a letter of guarantee provided by Directors of the Company, who are also Directors of Ocean and Oil Development Partners Limited (OODP), with significant shareholdings in Oando Plc,” Oando’s auditors said.

BusinessDay’s findings showed Ocean and Oil Development Partners Limited (OODP) owns 2,731,709,504 shares (representing 21.97% of the total number of shares) in the Company.

“OODP is ultimately owned 66.67% by the Group Chief Executive and 33.33% by the Deputy Chief Executive of the Company at year-end,” Oando said.

As at December 2026, Adewale Tinubu is the group chief executive of Oando while Omamofe Boyo is the deputy group chief executive.

Oando’s auditors also flagged a rare “Emphasis of Matter”, a mechanism used when accounting is technically compliant with international rules but conflicts with local law.

The issue centres on a shareholder who settled an outstanding loan by handing shares back to Oando itself, followed by a pro-rata redistribution of those treasury shares to other shareholders.

Auditors said that while the accounting treatment followed international standards, the transactions were not carried out in compliance with Nigeria’s Companies and Allied Matters Act and amounted to what the report called “impermissible returns of capital.”

“These matters have implications for compliance with statutory provisions relating to capital maintenance and equity distributions,” auditors said.

Two subsidiaries, Oando Oil Limited and Oando Servco Nigeria, forgave hundreds of millions of dollars owed by an entity called Whitmore Asset Management, even as the two subsidiaries carried accumulated losses of N257.1 billion and N536.5 billion, respectively.

Auditors said that in the absence of distributable profits, the forgiveness effectively amounted to a distribution out of capital rather than out of profit, again putting the transactions at odds with CAMA.

Oando Servco separately forgave an additional N447.9 billion owed by the parent company during the year, despite its own losses.