By the third week of every month, Ibrahim Olarinrin’s salary is gone. The 38-year-old Lagos resident earns N300,000 a month working for a professional services firm in accounting and finance. Yet feeding his wife and two children now costs about N360,000 monthly, more than his entire paycheque.

Once transportation, cooking gas, electricity, internet access and other essentials are added, the household requires roughly N462,500 every month before rent, school fees, healthcare or emergencies are considered.

Ibrahim lives in Fadeyi-Onipan with his wife and their two children, aged eight and five. The family occupies a modest room-and-parlour self-contained apartment. His wife supplements household income through a small home-based business, but even with two income streams, the arithmetic of family life has become increasingly difficult.

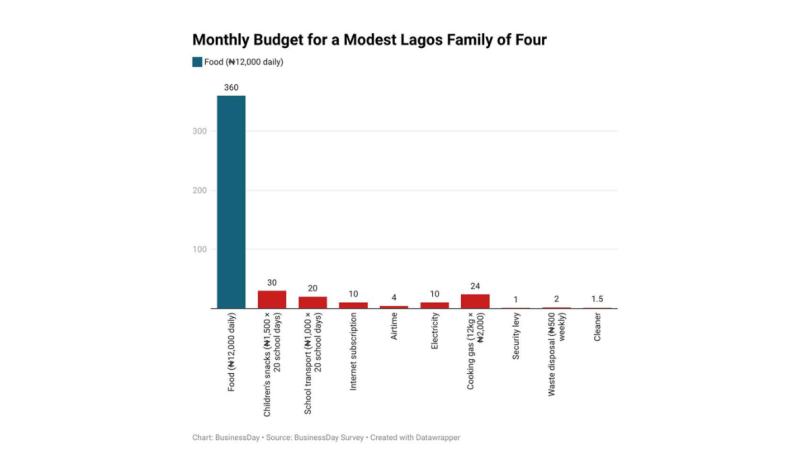

“On average, I spend about N12,000 a day on food alone for my family,” he said. “That does not include the children’s snacks, school transport, internet subscription, airtime, rent, electricity bills, cooking gas, security fees, waste disposal and cleaning expenses.”

At that rate, food alone consumes approximately N360,000 monthly, making it the largest driver of household expenditure. Basic living costs such as children’s snacks, transport, communication, electricity, and cooking gas add a further N98,500, while services such as security, waste disposal, and cleaning account for another N4,500. Overall, these expenses show how everyday consumption needs now absorb nearly all household income, leaving little flexibility for savings or unexpected costs.

The family’s recurring monthly expenses therefore total approximately N462,500. The structure of this spending highlights the dominance of non-discretionary items such as food, transport, and utilities, leaving limited room for adjustment. The figure excludes rent, school fees, healthcare, clothing, household maintenance and unforeseen emergencies.

Read also: Anambra workers lament N48,000 monthly salary deduction

Compared with Ibrahim’s salary of N300,000, the household faces a monthly gap of N162,500 before many major expenses are even considered.

His predicament reflects a broader shift taking place across Nigeria’s economy. For years, economic hardship was largely associated with unemployment. Increasingly, however, the challenge confronting many households is different. People are working, earning salaries and running small businesses, yet finding that their incomes no longer cover the cost of maintaining a basic standard of living.

The country is no longer confronting only a cost-of-living problem. It is confronting an income adequacy problem.

The rise of a survival wage

Data compiled from National Bureau of Statistics reports, market surveys and private-sector research suggest that a family of four in a mid-sized Nigerian city now requires between N349,000 and N513,000 monthly to meet basic living costs. Once rent and school fees are included, that figure rises to between N605,000 and N731,000.

The comparison with earnings is revealing. Nigeria’s statutory minimum wage stands at N70,000 monthly, while average formal-sector earnings are estimated at around N339,000 per month. In effect, what many analysts would describe as a household survival budget now sits at or above what the average salaried worker earns.

The implication is profound. A growing number of households can remain employed and still struggle to achieve financial stability.

This condition is often described as ‘in-work poverty’, a situation in which employment no longer guarantees economic security. While the concept is commonly associated with advanced economies, it is becoming increasingly visible in Nigeria’s urban centres, where the cost of essentials has risen far faster than wage growth.

The most important consequence of Nigeria’s recent economic adjustment is therefore not simply that prices have increased. It is that the amount of income required to sustain family life has changed dramatically.

How family budgets were reset

The years immediately following the COVID-19 pandemic were already difficult for households. Inflation was eroding purchasing power, but families could still rely on relatively stable fuel prices, a more predictable exchange rate and lower transportation costs. That changed after 2023.

The removal of petrol subsidies, exchange-rate liberalisation and the depreciation of the naira triggered a broad repricing of household expenses. Food inflation surged, reaching 40.87 percent in June 2024, according to National Bureau of Statistics data. Transportation costs increased sharply, while housing, education and energy expenses adjusted to a new economic reality.

Read also: LASG announces N50,000 salary support for workers

Although inflation has moderated from its peak, prices have not returned to previous levels. Households are therefore adjusting not to a temporary shock, but to a permanently higher cost structure.

The result is that expenses once manageable on a single middle-income salary increasingly require multiple earners, side businesses or significant reductions in consumption.

Why it matters

According to Muda Yusuf, chief executive officer of the Centre for the Promotion of Private Enterprise (CPPE), the erosion of household purchasing power is becoming an economic growth issue because families are spending a larger share of their income on necessities and less on savings, investment and discretionary consumption.

That matters because household consumption remains the largest component of Nigeria’s economy.

When families devote most of their income to food, transportation and utilities, less remains for healthcare, education, savings and investment. The consequences extend far beyond individual households.

Retailers face weaker demand. Small businesses struggle to expand. Household savings decline. Banks receive fewer deposits. Families postpone medical treatment and delay spending on education and skills development.

The erosion of disposable income also weakens social mobility. Households that spend nearly everything they earn on necessities have fewer opportunities to build assets, acquire homes or invest in their children’s future.

For policymakers, this may be the most important signal emerging from Nigeria’s inflation story. The challenge is no longer simply rising prices. It is the widening gap between what households earn and what everyday life now costs.

Ibrahim’s family is not unusual. It is increasingly representative of a growing number of working Nigerians whose salaries no longer guarantee financial stability.