BUA Cement Plc, the second-largest cement manufacturer in Nigeria, outperformed industry peers to become the most profitable cement maker by net profit margin in 2025.

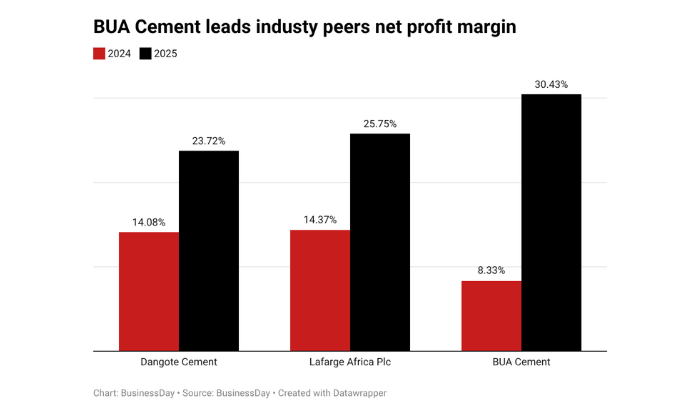

According to the full-year financial statements recently released, BUA Cement’s net profit margin jumped to 30.43 percent in 2025 from 8.33 percent in 2024, the highest among the three cement makers.

Lafarge Africa followed with a net profit margin of 25.75 percent from 14.37 percent, while Dangote Cement’s net profit margin improved to 23.72 percent from 14.08 percent.

Net profit margin tells you how efficient and profitable a company really is, after all expenses have been paid for.

A higher net profit margin means the business is keeping more money from its sales, while a low net profit margin means most of the money made is being spent on expenses.

The trio made a combined revenue of over N6.53 trillion in 2025, boosting their combined after-tax profit by 142 percent to N1.65 trillion from N677 billion reported in 2024.

Yusuf Binji, the managing director/CEO of BUA Cement, said, “At the start of the year, we outlined three key priorities: margin recovery, cost management, process improvement, and market penetration.”

“Through process reviews and targeted realignments, we explored smarter ways of operating internally. This approach included close engagement with suppliers and service providers across the value chain, and the results are reflected in the improved margins reported,” he said.

Read also: BUA Cement profit up 382% to N356bn, declares N10 dividend

Dangote Cement leads gross margin growth

Dangote Cement maintained its dominance in profitability, posting a gross profit margin of 62 percent in 2025, up from 54 percent in 2024.

This means the company retained N62 out of every N100 in sales before accounting for overhead and other expenses. The eight percentage-point increase reinforces Dangote’s position as the most operationally efficient among the major players.

Lafarge Africa also delivered strong gains, with its gross profit margin rising to 58.21 percent in 2025 from 49.71 percent in 2024. BUA Cement recorded the sharpest improvement among the three companies. Its gross profit margin rose to 51.62 percent in 2025, up from 34.25 percent in 2024.

How investors are reacting to the cement makers’ stocks

Investors are sending a clear signal to the market: confidence in Nigeria’s leading cement producers is on the rise.

Data compiled from investing.com shows Lafarge Africa’s share price surged 54.3 percent year-to-date, climbing from N134.5 at the start of the year to N210 by March 3. The sharp rally positions the company as the best-performing cement stock on the Nigerian Exchange within the review period.

Close behind is Dangote Cement, which posted a 33 percent gain. Its share price rose from N609 on January 2 to N809.9 as of March 3, reflecting renewed investor confidence in the blue-chip cement maker.

Meanwhile, BUA Cement recorded a 22.7 percent increase in its share price, rising from N178.5 at the beginning of the year to N219 within the same period.

For everyday investors, the reaction translates into swift capital appreciation in just two months. Someone who invested ₦1 million in Lafarge Africa shares at the beginning of January would now be sitting on gains of over 50 percent, excluding transaction costs

Industry analysis

According to the gross national product (GDP) published by the National Bureau of Statistics (NBS), the cement sector grew by 4.68 percent in the third quarter of 2025, compared to 2.6 percent reported in the same quarter of 2024.

A new report by policy think tank Agora Policy has attributed the persistently high price of cement in Nigeria to weak competition and market concentration within the industry, despite the country achieving self-sufficiency in cement production more than a decade ago.

The report stressed that the expansion of production capacity by major manufacturers such as Dangote Cement, BUA Cement, and Lafarge WAPCO has not translated into lower prices for households, builders, or government-funded projects.

The report stated: “Producers attribute high domestic prices to taxes, energy costs, transport challenges, and financing constraints, arguing that exports are cheaper due to exemptions from certain levies.

“However, this explanation raises a critical question: if costs are the main constraint, why are producers able to sell cement profitably abroad at lower prices than those paid by Nigerian consumers?”