In February 2026, the Central Bank of Nigeria delivered something that manufacturers, borrowers, and small business owners had been waiting for across nearly three years of unrelenting monetary tightening. The Monetary Policy Committee cut its benchmark rate by 50 basis points, from 27 percent to 26.5 percent.

It was a modest reduction, but it carried an outsized psychological significance. It was the first downward move after a cumulative 875 basis points of rate increases since May 2022. It felt, for a moment, like the beginning of something.

That feeling did not last long.

At its 305th MPC meeting, held on May 19 and 20 in Abuja, the Committee voted unanimously to hold the MPR at 26.5 percent. All other parameters were retained without exception: the Cash Reserve Ratio at 45 percent for commercial banks and 16 percent for merchant banks, non-Treasury Single Account public sector deposits at 75 percent, and the asymmetric corridor around the MPR at +50 and -450 basis points.

Olayemi Cardoso, CBN Governor, announced the outcome on Wednesday afternoon. The decision was not unexpected. What is becoming harder to dismiss is the cost of holding that line.

What drove the hold

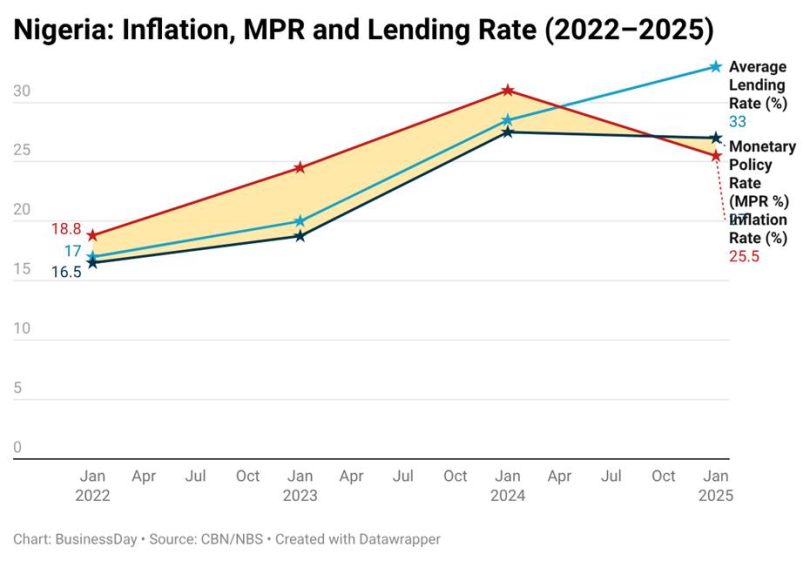

The MPC’s case for holding is grounded in specific data, and it is not unconvincing on its own terms. Headline inflation rose to 15.69 percent in April 2026 from 15.38 percent in March, the second consecutive monthly increase after nearly a year of declining inflation.

Food inflation climbed to 16.06 percent, surpassing headline inflation for the first time in eight months. The Committee flagged spillover effects from the Middle East crisis, which has disrupted global energy markets and pushed oil prices sharply higher, as a key driver of rising logistics and transportation costs.

Read also: Naira holds steady after CBN retains interest rate at 26.5%

External reserves stood at $49.49 billion as of May 15, still among the strongest positions Nigeria has held in over a decade, and the exchange rate remained broadly stable.

Against that backdrop, the Committee concluded that the inflationary uptick was externally driven and expected to be temporary. Core inflation, which strips out volatile food and energy prices, actually moderated to 15.86 percent in April. Month-on-month inflation slowed significantly.

The MPC judged that cutting rates into a supply-driven inflationary uptick would risk unanchoring inflation expectations at precisely the moment Nigeria’s credibility as an inflation-fighter had been established.

That judgment is technically defensible. Whether it is socially sustainable is a different question.

What the hold actually costs

The manufacturing sector, which the Manufacturers Association of Nigeria has documented is already spending approximately 40 percent of total production costs generating its own electricity, borrowed at an average commercial lending rate of 36.6 percent in the third quarter of 2025.

That rate has not improved materially since. A firm borrowing working capital at 36 percent annually, while simultaneously absorbing energy costs that account for nearly half its production expenses, is not a firm that can invest in expansion. It is a firm in operational survival mode.

Tosin Osunkoya, managing director and chief executive of Comercio Partners Asset Management, was direct ahead of the meeting. “I do not expect the CBN to cut rates anytime soon,” he said, arguing that persistent inflationary pressures, exchange rate concerns, and global geopolitical risks all counsel caution.

His projection proved accurate. What it means for his clients and for the businesses they finance is that elevated borrowing costs remain the baseline operating condition through at least mid-2026.

The CBN’s own April 2026 Inflation Expectations Survey offered a striking counter-signal. Of the 3,587 respondents surveyed, 63.3 percent said they wanted rates cut. Only 10.7 percent supported further tightening. The people absorbing these rates are not asking for patience. They are asking for relief.

The CPPE argument and why it matters

Muda Yusuf, ceo of Centre for the Promotion of Private Enterprise, has been among the most consistent voices calling for rate reductions, offered a measured endorsement of the May decision.

According to CPPE, the hold “reflects a pragmatic and increasingly sophisticated understanding of the inflation dynamics confronting the Nigerian economy.” Yusuf described the decision as evidence of policy maturity and said the MPC’s posture demonstrates “confidence in ongoing macroeconomic adjustments.”

Read also: CBN holds benchmark interest rate at 26.5% amid renewed inflationary pressure

That is a significant statement from an organisation that has argued persistently that high interest rates are structurally suppressing investment, constraining small business credit access, and limiting the productive capacity of an economy that urgently needs to grow its way out of poverty.

For CPPE to endorse the hold signals that even the most vocal proponents of rate relief recognise that cutting into an externally driven inflation uptick, with the 2027 election cycle approaching and fiscal pressure building, carries risks that the tightening itself currently avoids.

Yusuf’s broader message, however, was clear. The decision reflects progress in monetary management, but the real work is structural. Inflation cannot be sustainably defeated through interest rates alone when its drivers include food supply constraints, logistics bottlenecks, energy costs, and import price shocks.

“The outcome,” Yusuf concluded, “reflects a broader policy direction focused not only on inflation control, but also on sustaining investment, productivity, competitiveness, and job creation.” That is less a description of current reality than a statement of what the next phase must achieve.

The harder question

There is an asymmetry at the heart of Nigeria’s monetary moment that the MPC communique does not fully resolve. Financial markets, rating agencies, and institutional investors reward policy consistency and price-stability commitment.

They have done so. S&P upgraded Nigeria’s sovereign credit rating to B from B- in May 2026. Reserves are near historic highs. The naira is stable. From the market’s perspective, the CBN is performing exactly as a credible central bank should.